When Members are faced with ethical dilemmas the Code requires them to consider the following factors in determining the appropriate course of action:

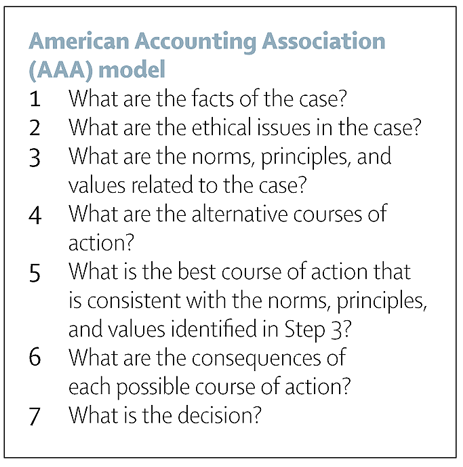

In practice, individuals will make decisions in various ways. A range of decision making models have been proposed over time to assist with such dilemmas. A commonly used model is the American Accounting Association (AAA) model. This model suggests a logical, seven-step process for decision making, which takes ethical issues into account. The seven steps are summarised in the image below and each step is discussed in detail.

- Relevant facts

- Ethical issues involved

- Fundamental principles related to the matter in question

- Established internal procedures

- Alternative courses of action

In practice, individuals will make decisions in various ways. A range of decision making models have been proposed over time to assist with such dilemmas. A commonly used model is the American Accounting Association (AAA) model. This model suggests a logical, seven-step process for decision making, which takes ethical issues into account. The seven steps are summarised in the image below and each step is discussed in detail.

The model begins, at Step 1, by establishing the facts of the case. While perhaps obvious, this step means that when the decision-making process starts, there is no ambiguity about what is under consideration.

Step 2 is to identify the ethical issues in the case. This involves examining the facts of the case and asking what ethical issues are at stake.

The third step is an identification of the norms, principles, and values related to the case. This involves placing the decision in its social, ethical, and, in some cases, professional behaviour context. In this last context, professional codes of ethics or the social expectations of the profession are taken to be the norms, principles, and values. For example, if stock market rules are involved in the decision, then these will be a relevant factor to consider in this step.

In the fourth step, each alternative course of action is identified. This involves stating each one, without consideration of the norms, principles, and values identified in Step 3, in order to ensure that each outcome is considered, however appropriate or inappropriate that outcome might be.

Then, in Step 5, the norms, principles, and values identified in Step 3 are overlaid on to the options identified in Step 4. When this is done, it should be possible to see which options accord with the norms and which do not.

In Step 6, the consequences of the outcomes are considered. Again, the purpose of the model is to make the implications of each outcome unambiguous so that the final decision is made in full knowledge and recognition of each one.

Finally, in Step 7, the decision is taken.

Step 2 is to identify the ethical issues in the case. This involves examining the facts of the case and asking what ethical issues are at stake.

The third step is an identification of the norms, principles, and values related to the case. This involves placing the decision in its social, ethical, and, in some cases, professional behaviour context. In this last context, professional codes of ethics or the social expectations of the profession are taken to be the norms, principles, and values. For example, if stock market rules are involved in the decision, then these will be a relevant factor to consider in this step.

In the fourth step, each alternative course of action is identified. This involves stating each one, without consideration of the norms, principles, and values identified in Step 3, in order to ensure that each outcome is considered, however appropriate or inappropriate that outcome might be.

Then, in Step 5, the norms, principles, and values identified in Step 3 are overlaid on to the options identified in Step 4. When this is done, it should be possible to see which options accord with the norms and which do not.

In Step 6, the consequences of the outcomes are considered. Again, the purpose of the model is to make the implications of each outcome unambiguous so that the final decision is made in full knowledge and recognition of each one.

Finally, in Step 7, the decision is taken.

The following two collaborative activities will give you practice in identifying ethical principles at risk and applying the AAA model to determine the appropriate course of action in each situation. These two activities require you to collectively create a GoogleDoc which contains a single comprehensive summary of how the AAA model would be applied.

|

Activity 5:

Access the GoogleDoc to apply the AAA ethical decision making model to the following scenario. Your analysis should include references to the Code where appropriate. |

Scenario

Howard is an accountant for a large firm of food processors. In the course of routine bookkeeping work he notices what appear to be regular cheque requisitions. The numbers seem out of sequence and the payee is an entity about which he has no knowledge. The documents supporting the cheque requisitions seem to be in order. He reports the matter to his superior, who says he will 'look into it'. Three weeks later, Howard asks the supervisor about the matter. The supervisor says, 'Oh yes, I looked into it. It's okay. Don't worry about it'.

Howard notices that the cheque requisitions continue to appear, always for large amounts and always payable to the same entity. He raises the matter with the auditor and is again reassured, after investigation, that everything is 'in order'. Howard is still worried by the matter and raises it again with his supervisor. The response from the supervisor is: 'I have already looked at it and it was okay. If you keep pestering me about it, I am afraid you will be looking for another job.' Howard decides taht discretion is the better part of valour.

A few months later, Howard's junior tells him that he has uncovered a scheme in which the auditor and senior management are siphoning large sums of money out of the business for their own purposes.

Howard is an accountant for a large firm of food processors. In the course of routine bookkeeping work he notices what appear to be regular cheque requisitions. The numbers seem out of sequence and the payee is an entity about which he has no knowledge. The documents supporting the cheque requisitions seem to be in order. He reports the matter to his superior, who says he will 'look into it'. Three weeks later, Howard asks the supervisor about the matter. The supervisor says, 'Oh yes, I looked into it. It's okay. Don't worry about it'.

Howard notices that the cheque requisitions continue to appear, always for large amounts and always payable to the same entity. He raises the matter with the auditor and is again reassured, after investigation, that everything is 'in order'. Howard is still worried by the matter and raises it again with his supervisor. The response from the supervisor is: 'I have already looked at it and it was okay. If you keep pestering me about it, I am afraid you will be looking for another job.' Howard decides taht discretion is the better part of valour.

A few months later, Howard's junior tells him that he has uncovered a scheme in which the auditor and senior management are siphoning large sums of money out of the business for their own purposes.

|

Activity 6:

Watch the following video (a bit dated!!) and access the GoogleDoc to apply the AAA ethical decision making model to the scenario presented. Your analysis should include references to the Code where appropriate. |

You should now move to the next tab "Ethics in the exam"